When the Powerball jackpot recently surged to $1.5 billion, “Powerball fever” swept across much of the country. On the news and across social media, many reported on what that much money (even after taxes) could buy, and the extent to which it could change a person’s life. I believe this helped people escape from the possibilities of their own lives—as well as their debt and their jobs—into a fantasyland where all one’s problems could be solved in an instant. Don’t get me wrong; it is great to dream. Let me ask you something a little more down-to-Earth: What would you do if someone gave you $25K to spend on anything you want? The only strings attached: you cannot invest it, save it, give it away, or use it to pay down debt.

Imagine that, unexpectedly, money has dropped into your lap. Maybe it is a gift, a prize, a bonus, or an inheritance. The ground rules are: you now have $25K to spend on yourself. If you do not use it to buy something, you lose it! If not, you must send it to me and I will spend it for you, on myself.

I realize that this is not a lot of money compared to the $1.5 billion Powerball jackpot, but for most of us, having $25K to spend on an item or experience is something pretty rare (other than buying cars or houses). How would you determine what to do with the money?

People are at different points in their financial and life journeys

I have seen people change from being spendthrifts to super savers and then finally to travel spenders during their lifetime. It makes a big difference where you are in your life journey. Factors include how frugally you have lived, your income, the amount you saved, how you invested, your savings, and whether you created a passive income stream. Each of us is unique and has a different background and approach.

Here are some rough categories I have noticed as stages:

Stage 1: When we are in our 20s, many of us are starting out in our careers and are at the beginning of gathering household basics such as furniture and other creature comforts. For many of us, these are the “spending years,” when only a small percentage of people save any significant amount of money.

Stage 2: By our 30s and 40s, we’ve typically progressed in our careers and are making more money. Most people are married with children at this point. These years are when many people mature financially and realize it’s time to start saving!

Stage 3: The 50s come around much quicker than you may realize. If you have not been saving and investing steadily for at least a decade, you may feel like you’ll fallen behind. Now it’s time to make some tough decisions and aggressively cut costs and save the difference.

Stage 4: For most of us, the period in our 60s and 70s will involve cutting back on work and eventually retiring. We will probably change from a saving-money mentality to actually spending part or our nest egg.

Stage 5: Our 70s and beyond—the “golden years”—is, for most Americans at retirement age today with little financial reserves, a time of living off the remaining few dollars saved and Social Security.

These are common stages for people in these age groups. Of course, there are many exceptions to this generalization.

$25K to spend: Do we spend it on things or experiences?

I have read several books and articles on happiness, in which the authors describe what seems to be the magical formula to obtain elusive bliss. They describe the psychology of our emotions. They often mention studies such as the Stanford marshmallow experiment. In this study, children from ages seven to nine who could wait for rewards instead of receiving instant gratification tended to be more successful in their lives.

Researchers have found that the idea—the promise—of buying that new shiny object or paying for a new experience is part of the happiness we derive from spending money. We see, even just a few months after a purchase, that sometimes the dream was actually more rewarding than the actual item or experience.

Experiences we have—vacations, family gatherings, milestone achievements—tend to stay in our memories longer than things. How many of us can remember the emotions we had about our third or fourth car when we are on our tenth vehicle? I have a hard time remembering what they were. However, I can still remember receiving a top science award in 8th grade, and I still have that award.

I have, though, had some excellent experience enjoying things. Sailing is a great example. I have had several sailboats that ranged in value from a thousand dollars into six figures. One of my most memorable experiences was sailing single-handed in a southern Colorado lake near sunset, enjoying a beer, and listening to the classic CSNY album Déjà Vu.

A great friend of mine found an autographed album by the group and gave it to me as a gift. It hangs to the right of my desk today.

The sailing example demonstrates how money spent buying a thing (along with the ongoing slip and maintenance expenses) produced a lasting memory. Ironically, this memory was in one of my least expensive boats.

A common conclusion that most authors on happiness reach is that often experiences result in more personal happiness than things.

$25K to spend: Do you have a YOLO or “life is long” mentality?

I mentioned in the You Only Live Once (YOLO) article last year that maybe we should consider living each day as if it were our last. Unless a person is on death row slated for execution, none of us really knows when our time on the planet will end. There is a limited amount of time for each of us, and the clock is ticking, and we had better get on with living the life we want.

“It comes down to a simple choice: get busy living or get busy dying.” – The Shawshank Redemption

However, wait, we have lots of life ahead of us! Why rush things and be in such a hurry? We can methodically save every penny over years… slow and steady is the course. Who knows about all the potential outcomes since this mentality encourages us to make more money, continue to save, and hoard every dollar.

Depending on your mindset, you may choose to spend your $25K on great experiences or buying something that you plan to own for many more years.

$25K to spend: How about using math to determine your decision?

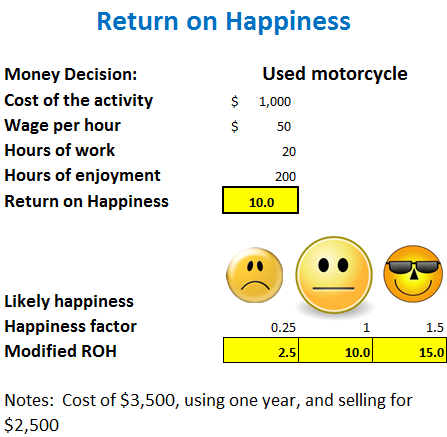

In an article on determining your Return on Happiness (ROH), I discussed how we could quantify the return on one purchase or experience compare to another. This was loosely based on the traditional ROI that many businesspeople use for measuring the best return on an investment for capital items or projects.

The formula for ROH involves the cost of the item or experience, your average hourly wage, the hours you have to work for the item, the period expected to enjoy the experience, and the level of happiness expected from the expenditure. It returns a likely happiness and added a “kicker” happiness factor to arrive at a final number. This is not too complex in terms the math, but could be confusing for some to follow my logic in quantifying happiness on purchases.

Here was an example I used looking at 1500 Days’ thoughts on buying a motorcycle:

Putting it all together

We are back to the original question of how to spend our mythical $25K. We have identified that the answer to the question will vary based on our age, the ability to wait, our desires for things or experiences, and our mentality about living for today vs. living for the future. Maybe we want to take the pure mathematical approach and quantify our happiness when deciding between multiple spending options.

I asked my wife this $25K question. She responded that she would take an extended and luxury vacation to a beachfront hotel in Tahiti. Since we have to spend all the money, we would be flying first class, enjoying butler service, daily massages, and offshore sailing. Of course, the food would be nothing less than 5-star quality. It would be a vacation to be remembered for the rest of our lives.

As for me, I would buy a fancy watch and use the rest of the money on multiple years of 5-star dining in Phoenix, Scottsdale, and the Sedona, Arizona areas. The watch would give me an object that is tangible, and intended to be left to my first grandson (if I ever have one), while the meals would provide years of enjoyment.

This demonstrates to me that answering my own question about how to spend $25K is not easy to do. I still wish to get as much value for my money and extend the experience as long as I can. I seem to be hardwired to shy away from splurging on just one experience or thing. This is the type of middle-of-the-road decision I usually find myself making:

Server question to me: “What size would you like, sir?”

Me: “Medium, please.”

My wife, on the other hand, would have no problem spending the entire $25K on one experience. This proves how different people are, even within the same household with similar dreams. One size or answer does not work for everyone!

Photo copyright : Ayelet Keshet (Follow)

You know what’s amazing? Financial Samurai made a post awhile back about what you would do with $10,000,000. A lot of people couldn’t think of anything specific, gravitating towards broad answers such as “I’d pay off my student loans, take a nice vacation, and then I don’t know.” Me on the other hand? I immediately without a second thought was able to detail an entire financial plan for every penny of those funds, complete with dividend investing, real estate investing, emergency funds, everything. All down to the penny. And then I was able to lay out exactly what I would do with my life after achieving financial freedom.

Here? With $25,000 and no saving or investing allowed? I honest to God cannot answer that question. I can bang out a financial plan for $10 million in minutes (and that’s no exaggeration. It took me literally less than 3 minutes to figure it all out in detail from scratch), but I could never figure out how to spend $25,000.

I don’t know whether that says something positive or negative about me, or at all.

Sincerely,

ARB–Angry Retail Banker

ARB,

It is weird that we can easily figure out how to spend a billion or $10,000,000, but we have a hard time with $25K. I believe that if we made the number $10K it would be just as difficult.

The $25K amount is something that is within many or our readers reach to receive. Perhaps it is some long lost relative passing away and leaving you money or your company went public and everyone gets bonuses. The fantasy of having millions allows us to dream a bit more and believe we can do everything we want now – since we are stinking rich. I plan on writing an article soon about how we spent $25K recently.

Take care and we will chat after the vacation.

I must be in a strange mood today. Normally, I’d be in ARB’s camp, unable to even start generating possibilities. Today my answer blinked its way out: “prepay my state taxes … for the rest of my life”. Prepaying expenses, with a potential for becoming a contribution if my wife decides we move out-of-state in retirement — hmm, maybe that fails the conditions.

Try again! I think I’d like to experience not worrying about yard-work or whether my wife skips the quarterly vacuuming again. $25k would cover ten years of twice-monthly service from gardener and housekeeper. Or twenty years of gardener service, in case she stands firmly to principle (and pride) by driving away the housekeeper.

Yeah. I’ll go with that.

Sabbaticalia,

Welcome to our site and thanks for commenting. I appreciate it! 🙂

Two things I like about you already: 1) you are in ARB’s camp (he does have a camp) and I am his number #1 fan and 2) you have the same dilemma I face with spending money.

I want to get all the possible value and utility from my purchases. The thought of prepaying for ten years of service is a good one. I thought I was being clever by dining out for 2 years, heck you get 10 – 20 years of value.

Take care,

Bryan

I should make my own camp. Like a banker’s boot camp or something.

Thanks for being my number 1 fan, Bryan!

Sincerely,

ARB–Angry Retail Banker

I think I’d probably use most (or all) of it for experiences, maybe travel related. At this point in my life, I have enough junk……er, I mean stuff…..and while it’s nice, it’s not the kind of nice that lasts forever (like the memories of a nice, top-rated trip). As I’ve gotten older, fond memories are more valuable to me than simply more assets.

Fun to think about!

John

I think you are in my wife’s camp with spending the money on travel related experiences. We also have too much stuff and now no real room to put store it in our downsized home.

For me it is going to be a combination of buying something and spending on experiences. (Medium please) This is a real life example I will be sharing in a post coming your way soon!

Hmmm does getting Tim’s dental implants done count as savings/debt? I’ll assume yes.

In that case, I’d take Tim on a nice vacation. For reasons too long to explain, our travel choices are a bit limited right now. So probably DC (he’s never been and there’s so much to see) or LA/Orlando (theme parks!!!!). For two weeks — don’t want to take too much time off work — call it $3k to stay in nice but not crazy nice hotels.

I’d get the garage set up to be a man cave for Tim with a pool table, which is his latest obsession. That’s more difficult than it sounds. We’d have to brick up the garage door, get a/c in there, maybe put a door in our dining room that leads to the garage. So call it… $5k-7k.

There are some upgrades/repairs I wouldn’t mind making around here. A few nice clothes for me in my new size.

That or take the money and try to get an adoption going. An older child, probably, given our health conditions and a few other factors that make us less desirable.

Abby, you have some low hanging fruit with the implants. I know that has been a goal you have been working on with Tim to achieve – with recent success. Wouldn’t it be great to be able to take that money to use on something else?

I like the idea of a “Man Cave” and other house projects. The adoption idea could be one of the greatest uses and gifts to a child. That one sounds the best!