In his bestselling book, The Automatic Millionaire, David Bach coined the term, “The Latté Factor.” In doing so, he prompted us to take a careful look at the impact of even the smallest purchases on our long-term savings.

The latté that so many people enjoy each day on the way to work took a head-on assault in the wake of this new concept. It has, no doubt, changed the way people view the cost of their daily habit. I wonder what it did to coffee shop sales!

For years, I lived by the belief that I should save every penny; the idea was: it would be invested and then, sometime in the future, I would become a multi-millionaire as a result of my latté-less lifestyle.

A few years ago, I changed my opinion about this strategy. I have come up with my own twist to this concept and coined it:

“The Reverse Latte Factor”?

David Bach wanted to prove that even small purchases add up over time. I get that. For example: if you spend $6 a day for a latté and a scone, five days a week, 50 weeks a year… that adds up to $1,500 a year. One way of thinking about this is if you simply put that $1,500 a year into the stock market, assuming you would make a steady 8% per year over each of the next 40 years, your investment would yield $388,585 upon retirement. Just like that, easy peasy! And all you had to do was give up a tiny bit of your daily routine—at least according to this school of thought.

One could say that most of the personal finance community can be placed in three broad schools of thought:

- Extreme frugality

- Extreme income generation

- A combination somewhere in the middle of these two paths

I have visited both ends of these extremes and feel that today I am near the middle, with a propensity to lean toward the frugality camp.

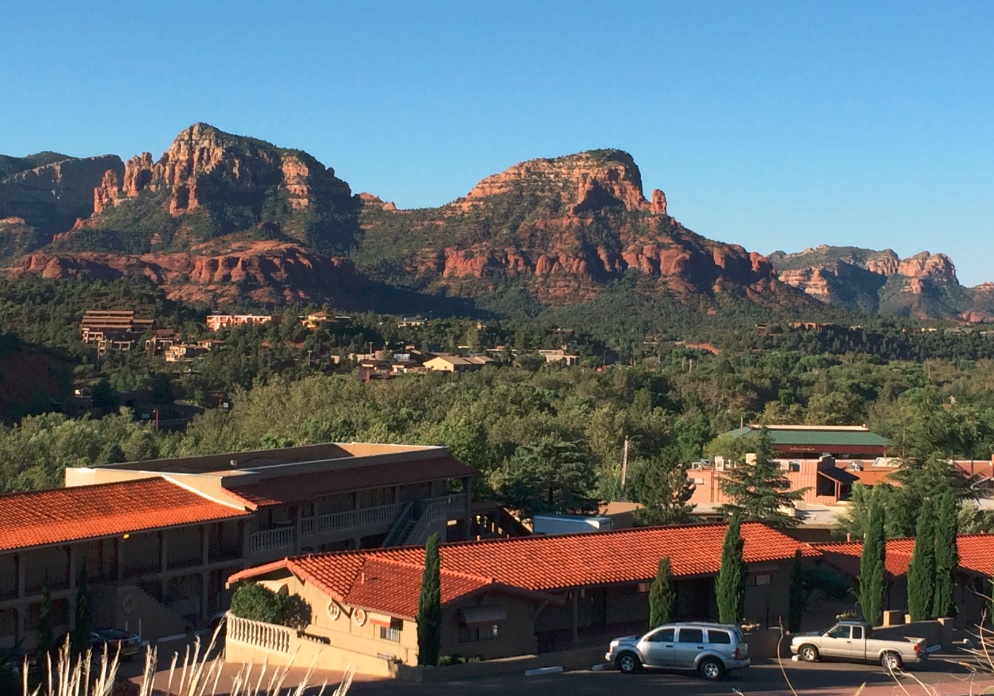

During the last couple of years, in the face of the stresses of work, in addition to aggressively saving and building my passive income stream, I have put many simple pleasures on the back burner. I changed that a few years ago when I realized that it is worth spending the money for an occasional coffee.

Take a look at the beautiful view I get for $4 a visit to my local Starbucks.

By the way, I find it really interesting how the folks at this location view Wi-Fi. I am guessing this won’t be a trend at other locations?

The Return on Investment (ROI) on the “The Reverse Latte Factor”

I work from home, with very little human contact. I can be on virtual meetings for most of the day, talking with people but not directly interacting with them. These days, the one with the most interaction with me is our cat.

So I began to take a reverse approach to The Latté Factor. What about looking at the maximum utility gained from small purchases? This concept was really brought home to me when I read Your Money or Your Life. In it, the authors put forward the concept of taking a detailed look at your expenses and ranking the derived value from each of those costs. It is broken down into units of measure based on the hours of your life working for your real wage, after considering the real costs of your job. I am now looking at this in a whole new way of creating an ROI based on units of time—or units of life.

Calculating the ROI on my coffee expenses

In my case, spending 50 hours a week in a home office and having no face-to-face human contact was driving me crazy. It was making me very cranky and, as such, re-affirmed my need to have some social interaction so that I would not have too many horrible Mondays. As a result, several years ago I began going to the coffee shop once a week to actively engage in conversation with people and hear their stories. I have now graduated to twice a week between two different coffee shops. Total expenditure: about $8 per week.

What is this $8 per week worth to keep a well-paid job for just one more year? How about spending $150 per week on a therapist to help me “find my center”? I could visit the coffee shop nearly 38 times for the cost of each therapy appointment. However, another way of looking at it is: if I stopped my $8 a week habit, I could have $103,623 saved if I earned 8% for the next 40 years.

I must add that my frugal side still shines through this tiny extravagance: I use the Starbucks app and a punch card from a local shop that gives me free items after a certain number of visits.

Today was extra special because I came up with this blog post idea while drinking coffee. I then thought, what the heck, I should go for a hike this morning. My normal early morning call was canceled so I leveraged that time into a hike. Take a look at the views.

A look south from Ridge Trail at Bell Rock (left) and Cathedral Rock (far right)

Here is what the trail looks like heading back to the trail-head:

Ridge trial heading north

This is another view closer to the end of the trail look toward West Sedona. We live near the bottom of the red rock formation on the far right:

Thunder Mountain is the largest rock formation in Sedona

ROI on the hike today

The Ridge trailhead is about two miles from my house. Yes, I did drive there! So let’s assume at a $.60 per mile cost, I have $2.40 in this hike. Heck, if I did the same trail five days a week for 50 weeks a year, I could save $600 per year in vehicle costs. Investing at an 8% return for 40 years that would net me $150,434 in today’s dollars!

I could have saved nearly $254,057 based on my twice-a-week coffee visit and my five-day-per-week hikes!

This math works very nicely if you are in your mid-20s and you plan on investing the difference for 40 years. What happens when you are in your early 50s like I am? The time horizon certainly has changed. I am of the opinion now that these small expenses are in alignment with my values. They have a very high ROI in the fact that they keep me from quitting my job now and, more importantly, away from the therapist’s couch.

So do we just not worry about The Latté Factor?

The book Your Money or Your Life really opened my eyes to evaluating my “enough” level for each of my spending categories. For some, travel is crucial while for others having a nice home is more important. Others may say that purchasing a new expensive car every few years is in alignment with their values, and worth the hours of work that they must put in for the benefit or trade-off of this expense. Who am I to say what is important to you? We each have to figure that out.

I will soon be reaching a new milestone in my life: I will be at a point at which I will stop saving a large percentage of my income. My W-2 earnings from a job will, at some point, cease and we will be living on our passive income. For me, now, the ROI is huge on having coffee twice a week and hiking.

If you are a 20-something, I would say that you need to look at even the small expenses. I highly recommend the exercise of looking at your expenses and evaluating a “what if” scenario if you invested the difference. It is definitely an exercise worth completing so you know how much impact even small expenses mean to your financial future. It can open your eyes to the idea that it is possible to find some fluff in your budget that can be put toward a goal of reaching financial independence. For the rest of us, though, it may be time to consider The Reverse Latté Factor.

Have you ever looked at evaluating the cost of certain expenses by ROI on your mental health? Have you read The Automatic Millionaire or Your Money or Your Life? If so, did they have an impact on your thinking about personal finance?

Bryan,

I think it really depends. Not all expenses are created equal, right?

I can tell you that I have some personal experience with this. The me of, say, a year ago wouldn’t have been caught dead in a coffee shop. I viewed it as a complete waste of money.

But now that I also work from home blogging, I started patronizing a coffee shop maybe six weeks ago or so. And I did it for the same reason as you – I was getting a little cabin fever staying indoors all day long. But since I started getting out twice a week or so, I’ve been more productive than ever. And that’s led to an increase in overall happiness and income. So the expense becomes an investment at that point, as funny as it sounds.

It’s funny because I just received an email the other day from a reader that criticized how my expenses have increased over the years. So they pointed out that the major difference was health insurance and hosting for the blog. Sure, I could cut them both out. But I’d be left with no blog and very little money. And no health insurance means I’d be paying a healthy chunk of change if anything happens. So just blindly looking at all expenses with a 1:1 ratio is a bad idea, in my view.

Thanks for sharing this!

Best regards.

Jason,

You absolutely got my point about how the small purchases really make a big difference in our lives, often times for reasons that do not have to do with saving money. This comment coming from a person like you, that lives very frugally compared to most, definitely validates the concept! Of course we are not going to act impulsive on too many small purchases. 🙂

Regarding your reader’s email: I too commented on a recent income update post of yours where you were doing an awesome job on increasing your income. However, I warned you to be careful to avoid the “old hedonistic treadmill” having an impact your life. You responded that you were “keenly aware of that lifestyle inflation. What’s great is that I’ve kind of “been there, done that” in regards to spending a lot more, and I still remember being less happy than I am now.”

I had totally forgotten about your story in Kraig’s podcast at Create My Independence regarding your childhood, family, inheritance, and early spending mistakes. It certainly has shaped your investment strategy. I truly believe it is experiences like those that will have taught us some valuable lessons, so history does not need to repeat itself. You are way ahead of the rest of the US population on your spending and savings habits.

Thanks for commenting!