My goal—and one that my wife and I share—has always been to be mortgage-free.

Although this has felt like a huge obstacle, it has been an important milestone in planning for our retirement.

Although this has felt like a huge obstacle, it has been an important milestone in planning for our retirement.

These days, the trend seems to be that more people are retiring with mortgage balances. To me, it appears fiscally irresponsible and risky to leave behind paid work as you get closer to traditional retirement age if you still have large debt obligations, such as a mortgage. This is, of course, a perspective coming from a person in my 50-something age group, nearing the end of a typical career. Those attempting to retire extremely early may have a very difficult time unless their mortgage is already paid off.

I was very close to having my mortgage paid off ten years ago. Then, things changed dramatically. A divorce from my first wife after 20 years of marriage certainly set back my ability to reach early retirement.

The great news is that my current wife and I reached one of our key personal finance goals when we paid off our home three months ago!

I find it fascinating to hear people’s stories regarding their big goals and what it feels like when they reach them. For that reason, we would like to share our experience.

We set a big goal: pay off the mortgage extremely early

One big goal was to relocate to northern Arizona, and it will be four years in October since we made that move. We had envisioned and planned for it over many years. We aligned our lifestyle, spending, saving, and investing with the goal of my wife quitting her job and both of us living on my income. Fortunately, my wife landed an excellent job locally and that made things so much easier for the transition.

When we left California, we rented our home to some awesome tenants. After 3½ years of discussions with our tenants, we worked through a deal to sell them our place. At the closing, we eliminated about 85% of our debt in one day. It took only nine years, from 2006 to 2015.

I’ve written before that we’ve been working on an enormous passive debt snowball that I started tracking in earnest years ago using an Excel spreadsheet. I later found a nifty mobile app for my iPhone called “Debt Free.” This is a great tool for analyzing different kinds of debt and evaluating “what if” scenarios of paying down debts in a particular order, the ability to use the snowball method, and options for making additional principal payments. Armed with that information, we were nonetheless torn between:

- Option One: pay off investment debt

- Option Two: pay off the mortgage

We chose Option #2: pay off the mortgage

There is a lot of discussion about the benefits and wisdom of paying down a mortgage. The common argument is that perhaps you should use that relatively cheap money to invest in other higher-returning investments such as the stock market. Or, quoting what Dave Ramsey often asked listeners of his radio show, “Would you borrow against your paid-for home to buy a rental property?” In the past, I would probably have said yes, but not today.

For us, there were no after-tax benefits because we were no longer able to deduct the mortgage interest. This was due to a combination of having a low balance and not enough other deductible expenses to get past the standard allowance. (Our other passive income investments are in a C-Corp that receives different tax treatment.) It really came down to an emotional decision for us—wanting to experience the feeling that comes from owning our home, free and clear of debt. Of course, even though we own the home, we also “own” property taxes, insurance, utilities, and ongoing maintenance!

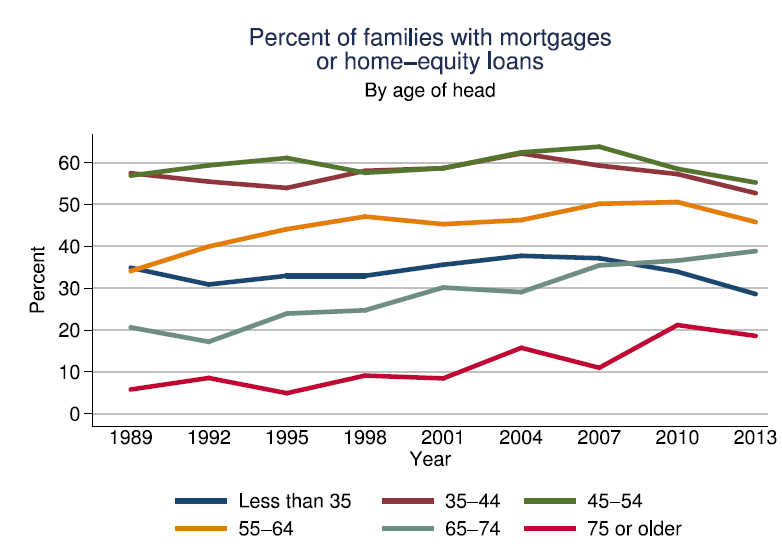

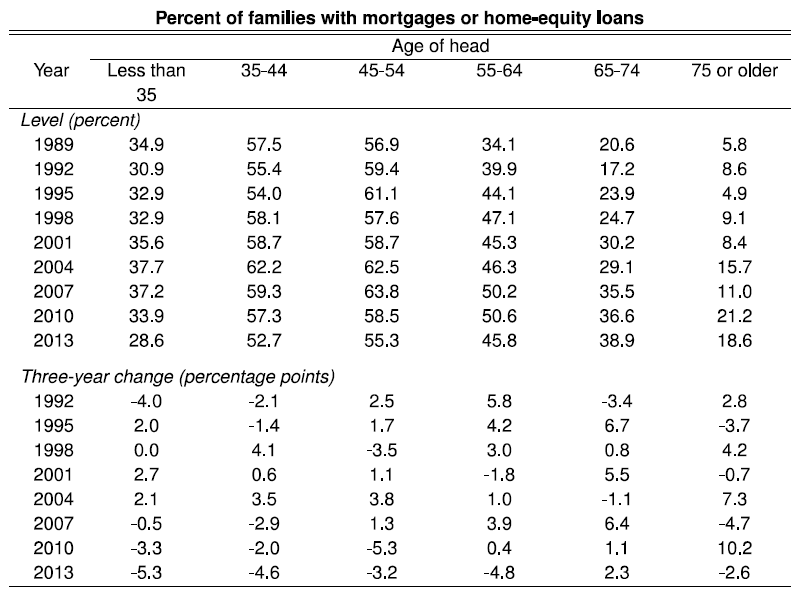

So, if you went with the argument about holding onto your mortgage as long as possible, why would you want to be like 45.8% of 55-to-64 year old people in the chart below who have mortgages? How would it help you to achieve early retirement any sooner?

I cannot imagine being 65 years old and having a mortgage. How about the 38.9% between the ages of 65 and 74 who still have mortgage obligations? That certainly cannot be a comfortable feeling, having mortgage payments at that age. I do have to point out that the general trend in the 2013 data for all age categories, except the 65-74 group, has been a reduction of families with mortgages or home-equity loans. Perhaps the data suggests people are beginning to see the value of a paid off home? (Then again, with the economy in its current state, it’s also possible that fewer people can afford to have a mortgage at all, and are renting instead.)

How it feels to have the mortgage gone

I have reached the goal I’ve had for more than twenty years: to be mortgage-free. Today, my wife and I are sharing what it feels like to have achieved that goal. There were many bumps and detours on my path to achieving this goal. I certainly didn’t have good luck or the best timing. We made many wrong financial moves by attempting to sell homes at not the best time or location. It was an outstanding day when our loan for the California property was paid off at the sale; we paid off our Arizona home, and directed the remaining balance to our passive investment debt. It really felt like a major financial accomplishment.

My feelings

I would have thought that my experience every day would be something like this: I wake up from a restful night of sleep, look at the awesome home my wife and I share, and feel overcome with joy at having the mortgage conquered. My experience was nothing like that. I think our focus has simply shifted toward eliminating the last of our business debt.

In hindsight, I have also had some second thoughts about paying off our home, strictly from a cash flow perspective. Had we paid off our investment debt, we would have more cash flow today. Instead, we now have 100% equity locked up in a non-liquid investment (our home) that provides us no ROI. Perhaps we have to measure it in terms of ROE (Return on Emotion), knowing we can live here forever, if we choose. Yes, we could use a HELOC or credit line to borrow against the home but that would put us right back into debt and defeat our original purpose. So, the real goal is getting to the bitter end of our debt snowball so we can enjoy the cash flow on the other side of this journey.

My wife’s take:

“My husband and I had been having daily discussions about paying off our home mortgage for years. These discussions would usually take place over morning coffee, while eating lunch, and often over dinner. I did feel immense relief once we sold our California home and subsequently paid off the mortgage on our current home in Arizona. This has been a huge milestone for us. I have to say the impact of having a paid-for home has helped me sleep better at night. What has been interesting is that because we are continuing our debt snowball we now seem to be having similar daily discussions about paying off our investment debt.”

All in all, it does feel great to have paid off the mortgage. We are both glad that day finally arrived!

There are a lot of options to consider when you run into a windfall of money, such as from selling an asset or receiving an inheritance. Is it wise to pay off a 4% interest rate mortgage, which is considered cheap money by historical standards, and invest it in Mr. Market when you can make 8% with no problem?

My perspective is that I should take the 4% risk-free option (mortgage interest rate) by paying off this debt now, as opposed to the uncertainty of trying to earn more than that guaranteed 4% return in the market today.

As a result of this milestone, we have permanently lowered our monthly living costs. This certainly is in alignment with our goals for financial independence and early retirement. We are now one step closer to the option of retiring early and pursuing our dreams.

Your story is really inspiring. As a young entrepreneur, I am now thinking of doing the same thing. I will definitely do something like you do.

Your blog is very informative. Thanks for sharing!

Thanks for stopping by! I appreciate the words of encouragement.

Hopefully the ideas and informative posts will keep coming. 🙂

Bryan,

Congrats on the amazing accomplishment. That’s really fantastic.

“So if you went with the argument about holding on to your mortgage as long as possible, why would you like to be like 45.8% of 55 to 64 year old people in the chart below that have mortgages? How is that helping you to achieve early retirement any sooner?”

That’s easily answered with math. If you can achieve a higher net return from investments, you’re better off keeping the mortgage and investing at that higher return. Seeing as how residential real estate has returned somewhere around 0% after inflation over the last 100 years and rates are so low now, it’s not a terribly high hurdle to clear.

“Had we paid off our investment debt we would have had more cash flow today. Instead we now have 100% equity locked up in a non-liquid investment (called our home) that provides us no ROI. Perhaps we have to measure it in terms of ROE (Return on Emotion) of knowing we can live here forever if we choose?”

That’s the flip side of the coin. You can’t measure the emotional satisfaction of having your home paid off in terms of dollars. If you would have achieved a higher rate of return and now have more wealth by investing more aggressively, would you be as happy ? Maybe not. You’re in a great spot, regardless! 🙂

Enjoy your paid-off home. Fantastic stuff.

Cheers!

Thanks for the encouraging words and insight. It is a great feeling having our home paid off! 🙂

You are correct regarding the return on real estate around 0% as an investment, once you correct for inflation. That has been my experience with the properties I have purchased. We have created a passive income stream with our rental properties for the cash flow aspect, realizing the actual appreciation of their value is negligible. We have been able to secure mortgages for these properties and collect rents to cover the operating costs and debt obligations. That debt is nearly gone as well. It is definitely the “get rich slowly plan”.

Our real estate portfolio is only one leg of our financial stool. We also have a large percentage of our net worth in mutual funds and stocks as well. That is why I am enjoying your blog posts and analysis of dividend producing stocks. This gives us some great ideas and another way of diversifying our assets into dividend stocks, providing us some additional passive income.

Take care!

It has been my goal as well during my life. I worked hard to pay off my apartment in Moscow 22 years ago just to move to US. After 11 years of renting (NYC!), moved to PNW and was focused on the house (no other debt had ever entered my life, thanks to my frugality and upbringing of the country where credit cards simply didn’t exist). A divorce (just like yours, 18 years of marriage), and during a market crash to add (2008) dropped a bomb on that dream. But with a new husband, who’s ideals are aligned with mine, we’re a short 3 years away to pay off our mortgage and move to a dream state for my part-time job (while he continues to work full time for a while longer). Glad I found your blog. Enjoyed the Reverse Latter Factor article as well.

Olga,

Thanks for stopping by and commenting. I love the pictures over at your site! It looks like we have a common passion – hiking!

It does seem that we have had some similar life experiences. I started over after 20 years of marriage. We both have certainly seen multiple crashes in our life. It is folks like you and your husband that can understand where we are in our journey. You are certainly facing the same questions and challenges.

I hope the content continues to be relevant and interesting to you. Thanks for subscribing. 🙂

Take care!

Congratulations on your fantastic accomplishment! I hope to join you by the time we are 50. Maybe it is a mid-life crisis but I am having a similar desire to move back to our families and friends. Our problem is that I have a job that I love and it is difficult to find the same kind of work where we are from. We will just have to tread water for a bit, but your story certainly gives me inspiration.

Jason,

Thanks for stopping by – I am glad you found us!

I loved your statement over at your site: “This blog is my journey trying to find “balance” between creating financial independence, peace in my work life, and sucking the marrow out life to its fullest”. I can’t agree with you more. I think you and I might be kindred spirits. 🙂

I do appreciate your comment regarding our accomplishment of paying off our home. It was a long battle that we were very focused on for years, finally coming to fruition!

The fact that you love your job is seems to be outside of the norm for people reading a blog like this one. I believe that you are one of the lucky few that found your true work. Congratulations!

Take care

We paid off our mortgage that we ever had in 2001, it was our first purchase. We bought two more brand new houses after that with all cash. I am 53 years old now and my husband is 57. We had been wrestled with issues you mentioned above, paying off the mortgage or invest in equity. I decided to pay off the mortgage. We refinanced our 30 year to 15 year later on and made three payments every month mostly. It took about a little over seven years to pay off. At that time, stock market was doing very well, yet there is no guarantee in stock market. On the other hand, I knew what I was getting exactly by paying off mortgage early and it was guaranteed. Right after we paid off mortgage, 9,11 in 2001 happened. I don’t have to tell you what happened to the stock market after that. My financial motto is “never to gamble with fundamentals. We had a very good deal on second home purchase, cash purchase gave us negotiating power.

Young,

That is awesome that you paid off your mortgage 14 years ago. What an accomplishment. I am doubly impressed that you paid cash for a second home. I have never bought a house outright for cash. We have come close, but never quite there.

BTW – I know exactly how you feel about having a paid off mortgage instead of more money in the market.

It seems your situation and ours are very similar. I would be curious to hear what you are going through on deciding where to live, your plans for RV’g, and what is driving your decision on when to retire? Those are normal conversation topics for us in this house! 🙂

Would you be up for a guest post to tell your story?

Take care,

Bryan