In books on personal finance, the chapters are typically organized in a fashion that takes an overarching, holistic approach to the financial aspects of your life. The authors describe how each concept—determining your net worth, creating a budget, having insurance, planning for taxes, creating a will, and the hundred other things we should be doing—relates to your overall financial picture.

(Attempting to tame those snarling budget categories)

I would like to take a different tack and outline what I believe are the mechanics of getting to financial freedom or financial independence. My goal is to distill down a lot of information and create a “financial independence hack” to demonstrate some fundamental tasks you must do in order to get there—and, more importantly, to know if you have arrived. So things like insurance and wills won’t be touched upon other than mentioned for budgeting purposes.

This will be the first in a series of seven articles that will discuss what it takes to reach financial independence and how to determine the criteria for success. I hope you enjoy the series.

Now let’s tackle Step One, Budgeting!

Making a budget is a “pain in the butt” – Do I really need to do it?

For many, the task of creating a budget brings up some very negative emotions. Perhaps you don’t like to look at your finances in general, have no interest in numbers, feel depressed that you are not financially savvy, or have serious financial problems. The list goes on! Believe it or not, other people (including me) actually enjoy working with numbers, so for us this is not a big deal. However, I recognize that for many, it is.

Much of the personal finance literature talks about budgeting and the reasons it is so important. To me, the biggest reason, learned from years of practice, and working in finance and accounting, is: “You can’t control what you can’t measure.”

A budget tells us what we can’t afford, but it doesn’t keep us from buying it.

—William Feather

It is interesting to see that writers have begun to use weasel words like “spending plans” so that we don’t have to mention the “B word”, budget! You would think they are describing disease or death. For the sake of my sanity, going forward on this blog site, let’s just call it a budget. J

Creating a budget does take time, especially when you are beginning the process. If you have not created one before, the task may seem daunting. People avoid this because of the pain or stress that it generates, and I certainly understand. The challenge is that, in order to achieve a lofty goal of reaching financial independence, coupled with retiring early, you cannot skip this step. The research that Thomas J. Stanley and William D. Danko completed for their best-selling book the The Millionaire Next Door shows that millionaires typically spends 4.6 hours per month on their personal finances. Another interesting fact: millionaires are mostly likely to drive a Ford F-150.

Why wouldn’t you invest the time in yourself to practice millionaire habits? Fake it until you make it, baby! Hang in there, because it does get easier as you go. No one is born with the knowledge to create or abide by a budget; it is something we all must learn. You can quickly turn budgeting into a habit once you understand and implement this process.

A common question people ask is this: What about my spouse, I can’t seem to get him (or her) on board? My response is that you must “be the change” by creating a budget on your own if necessary. I recommend that you discuss it with your spouse and share your reasons to bring him or her into the decision-making process. Explain to your spouse why it is so important to you. Gain buy-in by showing the possibilities of what can be achieved with a little focus and with follow-through on reaching your goals together. Consistency and tenacity with results will ultimately win your spouse over.

If you are new to budgeting, you need to do some work up front.

I would assume that most people are familiar with a budget. It is a means of tracking income and expense items by category. There is probably an infinite number of ways one could categorize each expense.

For example, let’s discuss just one item: food. To me, food can fall into the categories of entertainment, restaurant dining, travel, or groceries. I do my best to identify a logical category that I use consistently. When we go camping, the food for the trip is considered groceries, since we either eat at home or in our trailer. Stopping at a McDonalds on the road somewhere on the way we call “dining.”

The secret to budgeting is to be consistent so that you can compare trends over time.

When you consistently categorize your expenses the same way to the same category, you have the ability to conduct some historical analysis of your spending habits. I suggest using around twenty groups that you can consolidate in your budget. Each person needs to find what works best for him or her. This will undoubtedly change along the way as you fine-tune the process.

Here’s how we arrive at our monthly budget.

My wife and I go through a process every month to create a plan for where every dollar goes. This has been further enforced, for me, by being a Dave Ramsey fan.

I first started budgeting years ago, with five- or seven-column pad accounting ledgers, then spreadsheets, then moved on to a software program called Managing Your Money, and finally arrived at Quicken. (I just dated myself.) I know that many people rave about Mint but I have not found the need to make that jump. So far, Quicken does what we need.

We have linked all of our accounts in Quicken to do a one-step update. This software will grab all of the latest transactions from our accounts and drop them into a que for our review. I also enter the two to three monthly checks we write. I have numerous recurring transactions like our paychecks, monthly transfers, and savings set up automatically.

We have tried to streamline everything we can to be simple, and automate what is remaining. This was really brought home after reading the The Four Hour Work Week multiple times! Make sure you read the chapters on elimination and automation. We have cut down significantly on the number of bank accounts and credit cards to further simplify our lives. However, we do still maintain numerous accounts to “fund” some large purchases or savings goals.

Each month, I run a customized Quicken report that summarizes our spending. I have a spreadsheet (I can already hear it now about not using Quicken’s budgeting tools) that I use to show the current month’s plan budget and an “actual” column where I enter our actual expenses. We then look at the next month and project our spending using the previous month as a guide—and taking into account any other expenses we may incur for the month.

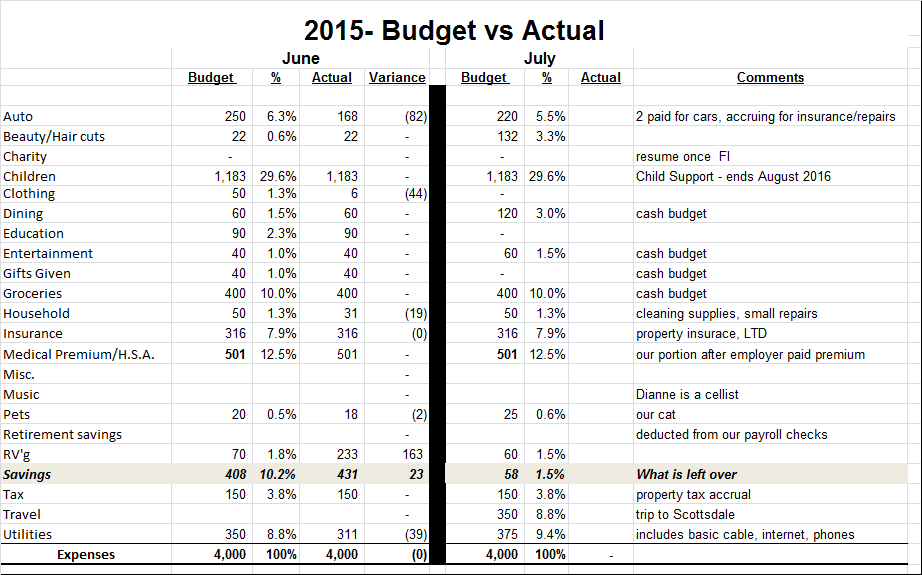

Here is our current budget:

To me, it is always fascinating to see how people spend their money. Taking a look at our numbers like a forensic accountant, one might draw some conclusions. I made some notes on many of our spending categories. Certainly you have questions, such as do we make $4,000 a month? My commitment to you is that, to everyone who asks a question in the comment section, I will respond back to your question the best I can, short of giving away too much personal information. 🙂

That’s all there is to budgeting!

I mentioned at the start of the article that this is the first of our seven-part series of the journey toward financial independence. I encourage you to check back for new updates over the next six weeks.

Budgeting is a great way to consciously determine a “home” for your dollars each month. It is a tool in your early retirement toolbox that will enable you to understand where your money goes and to properly align your goals with your spending. I hope this has awakened something in you, if budgeting is not already part of your financial planning today.

This is a crucial step in the early retirement journey that I believe cannot be skipped if you wish to achieve above-par results in a shortened timeframe. I do not know of a single person who has reached financial independence who did not spend time each month on this activity.

Disclaimer: I also don’t know any lottery winners.

Budgeting is a tool that can help you create financial control habits and it provides a historical record of your income and costs. This will go a long way to help you predict your living costs and determine when you have reached your personal point of financial independence.

Nicely done. I’m a big fan of budgeting. We buget on a monthly basis, and it has been by far the most impactful habit we picked up after getting married.

We do track – but do it passively. We use the envelope system so there really is no tracking per se. It’s worked out great. Other than small “emergencies” we havent deviated since we’ve been married (2 years)

The paradox of our budgeting is that we are very strict and at the same time very loose. We always hit our goal but spend zero time stressing or worrying about it. That’s the power of a budget!

Luke,

It is great that you have discovered some benefits to budgeting each month. Especially early on in life! For me the action that really helped is when we reviewed our actual expenses to what we budgeted. It made us very aware of where our money leaks were and how we should plug them.

I like the money envelope method because it requires less transactions and tracking in Quicken. We start with an amount each month for those categories and withdraw the cash from the bank. Peeking at the envelopes during the month gives us immediate feedback as to how much we have left to spend. Using a debit or credit card makes it too easy to buy and overspend. 🙁

Take care,

Bryan

We use a zero-sum budget. We create a new one at the 1st of every month, and do our best to live by it until the next month. It works great 99% of the time, and has made a huge difference in the amount of money we have been able to save over the years!

Holly, we are using a zero sum approach as well in that we start with a fixed income and all our dollars must have a named home or category where they will go.

I know for you and Greg your budget is based on your prior month’s income. That is a smart move for people that have variable incomes that change from month to month. It makes it so much easier to not overspend since you know what your income was for the previous month. It also is a great way to have an extra month buffer of cash in your bank account.

Thanks for the comment and take care!

Hi Bryan,

First time I’ve come across your site. Great post! I got a lot out of the Millionaire Next Door book, as well, and hope to apply some of their lessons to my every day life. Your article has great advice. As you mention, budgets are not fun – initially – but after doing it for a while and seeing where we can trim our expenses, I almost look forward to revising them to see how much more we can save.

Keep up the good work! I hope to one day retire early, as well.

-DP

http://www.somedayextraordinary.com/

DP,

Thanks for discovering us and commenting!

It is amazing how many times I have mentioned the Millionaire Next Door in my posts. It really became apparent as I went back through and started adding some Amazon Associates links to past articles. The big take away point from this book; these millionaires really lived a very non-flashy and conservative lifestyle.

If you have not already read Your Money or Your Life, I highly recommend it. I suggest you check it out at the local library if you can. If one is not available, a shameless plug on my part, please click the link on my resource page to buy a copy from Amazon. Either way, I am curious if you have read the book and if so, did it have an impact on you?

Take care,

Bryan

Bryan,

No problem with the shameless plug – I’m all for that! I actually have not read Your “Money or Your Life” yet – I wasn’t even familiar with it until you mentioned it. I will certainly add it to my list, though. If you have a chance, feel free to take a look at my resources page as well. There might be something there that catches your eye. It’s a little investor heavy as that is my main reading focus.

Thanks for the recommendation and the comment back! I’ll definitely take a more in depth look at your page.

-DP

Excellent post. I have started a budget too that is very aggressive. I’m starting off aggressive because over time, I can always relax the constraints. I hope to achieve the rest of my 2015 goals this way of paying off my student loan and building my savings account!

Have a good day,

Erik