This article is the third in a series of seven that will discuss our approach to reaching financial independence, and determining key criteria for success. If you have not already read the second step covering passive income, please take a minute to visit that post. This article will discuss why you should calculate replacement and maintenance costs into your budget on your financial independence journey.

In Step 1 we communicated the many benefits of setting up a budget to take control of your financial life. The Step 2 article discussed why it is so important to have a side hustle and create a passive income. These steps should help awaken us to the fact that if we do not manage our expenses and design income independent of work, we may be choosing a long and rough road to achieve financial independence.

-

Some of these might need replacing

Often our focus is directly toward living frugally and well below our means, aspiring to reach a crossover point where we can stop working. It is easy to fall into a trap of saving your money and believing your possessions will last forever.

When you hit FI or retirement, it does not necessarily mean that you are done with saving and expenses. We do not achieve that storied fairytale point of financial independence where we have everything we will ever need, and we can simply live the rest of our lives with what we own.

Perhaps as we get much older, we will no longer have to purchase or repair as many things that we own. However, for recent retirees in their sixties, retirement can last a long time.

Step 3 will discuss the need to understand replacement costs and maintenance. We will explore these considerations and come up with a plan to accomplish our goals of financial independence and retirement.

You may be retired for decades. Items WILL need replacing.

I enjoy reading personal finance blogs, financial articles, and books. I have extracted at least one tidbit from every personal finance book I have read. The core of my financial direction and foundation has been highly influenced by people on my blog roll and authors I have listed on my resource page.

Earlier this year, I checked out a book from our library. Although it was written in 2014, it recently appeared in our library as a new release. Something new to read! I have consumed the entire PF section of the Sedona Library and the title caught my attention:

The 5 Years Before You Retire, by Emily Guy Birken

Wait a minute, I thought, I am five years before my retirement so this person must have written this book for me!

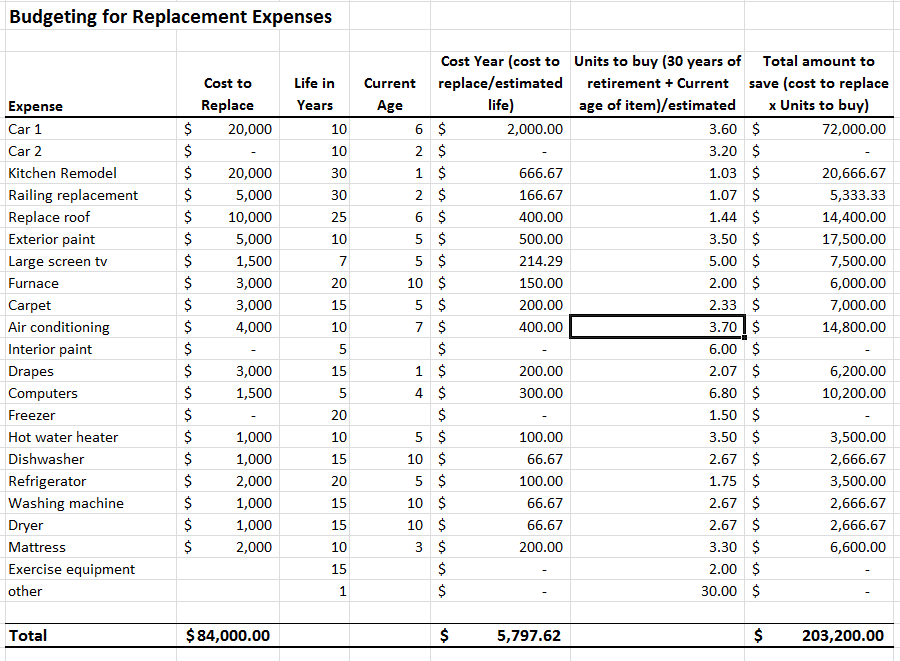

In her book, Emily discusses an important aspect to retirement that I had overlooked. We need to consider all the items we may end up replacing and maintaining over a potential 30-year retirement period. This retirement period could be much longer for those extreme early retirement movement folks in their twenties and thirties. Can you imagine how many items ne ed to be replaced during 50 years of retirement?

ed to be replaced during 50 years of retirement?

Some examples for homeowners include: furnaces, AC units, roofs, kitchens, bathrooms, carpets, and appliances. For both the renting and homeowner crowd we have to consider replacing vehicles, TVs, furniture, computers, and the latest tools, gadgets, and time-saving devices.

The remarkable learning moment for me came when I realized that these items have different lifespans, costs, and replacement periods.

For us accounting nerds, we would call this “book value”—the asset’s useful life, and depreciation. My business life and personal finance life do not always communicate well with each other. 🙂

In our case, some of these items were at the beginning of their lifecycle while others were near the end. I created a spreadsheet from Emily’s example that reflects the projected cost for our situation.

The very action of going through this process, listing all these future expenses, helped me see how unprepared I was for these costs. I may be buying six or eight more cars. We might need seven more computers. There needs to be $203K available to manage our replacements. Zoinks!

But wait, there’s more. What about our bucket list? I had better understand what our bucket list items are going to cost and factor those costs into our planning.

What’s on your bucket list?

A great movie by Rob Reiner is The Bucket List, released in 2007. The movie followed two people with terminal illness. Their prognosis helped them narrow their focus very quickly to determine what was important in the remaining days of their lives.

It was time for them to determine the most important experiences in life. One of the characters was quite wealthy so he covered the cost of their escapades, enabling them to cross off one item at a time from their bucket lists.

I can only imagine what it would be like to know one has limited time left. No need to waste any more time to get things done, dreaming about that elusive “someday.” This certainly would lead you to determine your priorities, realizing you cannot do everything, only what is truly important.

This also forces a person to understand your “why” and the motivations around your goals for your bucket list. It brings clarity to the purpose of and reasons for achieving goals that are so important in your life. It makes you ask the question: Can you be content without completing all of your bucket list items?

The real message is that we all have limited time. None of us really know when our time will be gone. The clock is ticking away and we cannot get any of our time back. What would be wrong with taking the time now to identify and chart out what you want to do with your life? How about determining places you want to visit or live, an interest you wish to study, hobbies to pursue, people you want to meet, things that you would like to own, charities to support, or building the legacy you wish to leave?

What do you expect to do with the rest of your life?

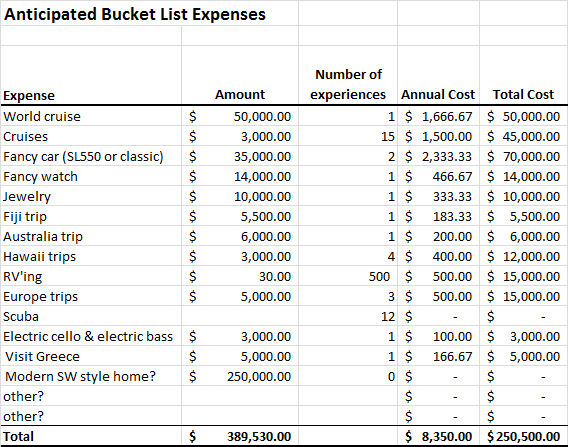

Dianne and I have some big dreams and have confidence that we can achieve our goals. We have created dozens of lists and plans for the future. We have reflected our current plans in our bucket list:

Our bucket list costs based on 30 years of retirement.

This was a thought-provoking exercise for us to identify costs and the number of experiences for our bucket list items. Another revelation: we need $250K to fund our bucket list. Yikes!

Note: neither our replacement nor bucket lists factor in inflation. So this could get much more expensive!

How about you, do you know what it will cost to do all the things you want in your life? Try out this approach of listing bucket-list items and identifying what they will cost. This can then be the start for your long-term goal setting.

Understanding your bucket list and replacement costs

Step 3 in our financial independence journey is an important planning element that will help you visualize your future experiences and understand replacement-related costs. This underscores the importance of Step 1, budgeting and managing your expenses. Financial  independence or retirement may never come without some work in those areas.

independence or retirement may never come without some work in those areas.

More importantly, what would be wrong with having some fun budgeting for your bucket list items?

We know from Step 2 that saving and investing can turbo-charge your results, building a passive income to sustain your day-to-day living expenses. There is hope for having the ability to fund your replacement and maintenance expenses by saving and investing wisely. This will require a strategy of creating a passive income stream and nurturing its growth potential for early retirement.

You might wonder where all these steps are leading. No worries, I will connect all of the dots in Step 6: Achieving Financial Independence. This will include a working spreadsheet for anyone interested in taking the accountant’s perspective toward reaching financial independence.

We welcome you to check back next Thursday for Step 4: Test Drive Living on Less Income.

Have you created a bucket list with time-frames and costs for the rest of your life? Are replacement and maintenance costs something you have factored in to your FI number?

One more year thing is going on with us. RVing for a while till we find a good place to retire and buying a house for the last time. This was my original retirement plan but I’m having a second thought recently. there are so many beautiful countries and so inexpensive these days, so tempting, even though I’m not adventurous. My husband should been retired in 2014, yet still working. I’m going through changes that make me tired and cranky. Retirement plan is the only thing will not turn out as I envisioned. I don’t really think about replacement costs. Like you wrote, they have different lifespan. Our retirement is mysterious even to us at this point. I like to find something that generates extra income after retired by doing something together, but My husband’s definition of retiring is doing nothing.

Young,

Thanks for stopping by!

Your story does sound similar to us. I can certainly understand how your husband should have retired, yet continues to work. We have been at this journey so long it does not seem to have an end.

These replacement costs and actual bucket list items have become an important element for our retirement plan. We have to prioritize what is important and save for those experiences we wish to have and the stuff to replace. The underlying fear of course is not having enough!

I appreciate your feedback and sharing your situation.

Take care,

Bryan