This article is the sixth in a series of seven that discuss our approach to reaching financial independence, and determining key criteria for success. If you have not already read the fifth step, about becoming debt free and celebrating freedom, please take a minute to visit that post. This article will discuss how to determine when you have reached financial independence before retirement.

To recap, in Step 1, we outlined the many benefits of setting up a budget to take control of your financial life. In Step 2, we discussed the reasons it is important to have a side hustle and create a passive income. In Step 3, we covered the need to plan for replacement and maintenance costs in the journey toward financial independence and retirement. In Step 4, we explored the concept of “test driving” living on less income. In Step 5, we reviewed the importance of becoming debt free and the impact it has on financial independence and retirement.

These steps illuminate that if we do not manage expenses and design income sources independent of work, we may be choosing a long and rough road to financial independence. Now we’ll take a look at how much money is required for financial independence in our early retirement plans and how to know when we have succeeded.

Your spending will determine your Financial Independence Number.

Knowing your spending is crucial to determine your Financial Independence Number. If your spending is unknown, inconsistent, or simply out of control, it is difficult to determine how much is enough for retirement. Following a detailed budget and tracking your spending, as described in Step 1, provides a roadmap to your expenses and lifestyle.

“Would you tell me, please, which way I ought to go from here?”

“That depends a good deal on where you want to get to.”

“I don’t much care where –”

“Then it doesn’t matter which way you go.”

― Lewis Carroll, Alice in Wonderland

To become debt-free requires following a budget, saving, and building a passive income stream… each requires discipline. Without having learned to live within one’s means, planning for financial independence is nearly impossible.

Predicting your Financial Independence sources of income.

It’s important to invest and set up future sources of income, such as:

- A passive income stream. This could include rental real estate, dividend income, stock investments, and bonds.

- Savings. Savings accounts and funds set aside for specific purchases.

- Part-time work. This could include part-time, contract or temporary work.

- Roth, 401k, IRA retirement accounts. Money saved in employee or individual retirement accounts.

- Annuities. The use of an insurance product to create a guaranteed income stream for a period of time.

- Social Security. This can be accessed as early as age 62½—or earlier with a qualified disability.

- Pensions. A company-sponsored program that could provide additional retirement income; these are, unfortunately, going the way of the dinosaurs.

Timing of income and expenses are crucial to plan for cash flow.

There is a movement in the United States among many frugal-minded folks to retire quite early. The retirement ages for these people are often in the thirties or forties. The early-retirement crowd will need to plan for living expenses lasting decades without the ability to draw on Social Security or pension incomes. Understanding how your income sources match up with expenses once work stops is important to make sure you do not run out of money before you run out of time.

We expect our spending will be greater in our early years of retirement and decline in our later years. Many of our bucket list items involving RVing and travel are likely to happen earlier in our retirement, rather than later. The passive income and side hustles are initially the most crucial income sources for those years before drawing on Social Security or company pensions.

We presume that once our “travel bug” has run its course, other costs will soon begin to increase. These could involve projects like remodeling our existing home, upgrading to a new home, or increased medical care and more social and community-based activities.

What does your financial independence cost?

We can anticipate our Financial Independence Number, deriving it from years of budgeting and the specific costs we expect in retirement. Here are the tools we are relying on to predict our expenses:

- Retirement budget. The post-work budget based on normal living expenses.

- Saving funds. Money set aside for specific spending purposes. This includes taxes, insurance, and an e-fund.

- Savings due to retirement. This is where you can lower your budget, taking into account what will be saved by retiring (commuting, clothes, cars, etc.).

- New retirement costs. We anticipate that we may join clubs, gyms, and other organizations.

- Replacement costs. The costs we discussed in Step 3 to replace those appliances, floors, cars, and other things that wear out.

- The bucket list. The list of those items important to us—things that we want to do before we leave this planet.

The 4% Rule for safe withdrawals.

It is time to grab another piece of the financial independence puzzle. This is commonly referred to as “the 4% Rule.” This rule was established through a Trinity Study using Monte Carlo simulations to determine the probability of your life lasting longer than your retirement account balance. That is always a good thing—to outlive your income! 🙂

The quick and simple “rule of thumb” is you can withdraw 4% of your nest egg balance each year and never run out of funds.

Dianne and I are quite conservative, not the most frugal with our spending, do not plan to receive income for work after retiring, and wish to use a 3% withdrawal rate for our planning. We also have additional income streams that will include pensions and Social Security that we are not factoring into our Financial Independence Number, therefore providing an additional safety buffer.

Several blogs I follow have explained this 4% Rule quite well, discussing how it affects planning. I recommend you check out their articles:

- Go Curry Cracker: Jeremy discusses how the 4% Rule has become an endowment fund.

- Think Save Retire: Steve is using this rule as a guideline.

- 1500 days: “Why dinosaurs will eat you if you follow the 4% Rule” (taken out of context) 🙂

Let’s put the financial independence numbers all together.

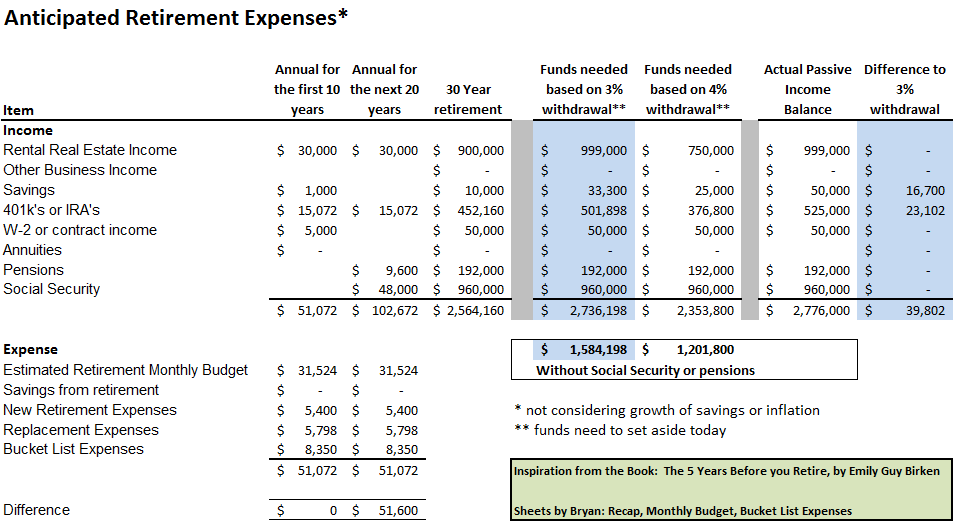

The saying goes that a picture is worth a thousand words. Then how about we provide a picture of a spreadsheet? This is a simple spreadsheet created for our income and expense planning. More importantly, we are using it to determine whether certain passive income streams are enough to fund the lifestyle we wish to enjoy in our extended retirement.

Do you know how much is required to afford your early retirement lifestyle?

We have determined that, for our first 10 retirement years, the expenses will be $51,072 annually. This is a more “lavish” budget than many in the extremely frugal camp would have for their expenses. For us, these numbers include and represent the costs to replace items, take on new hobbies, and allow for our bucket list items. All of those expense numbers are linked to separate tabs of this spreadsheet.*

Note: The passive income balances are not our actual numbers but used as an example to show sources of funds needed to cover our anticipated expenses.

Let’s do some analysis on a couple of numbers as an example. Using the more conservative 3% as a guide, we would need to have saved $278,055 to pay for our bucket-list dreams.

However, using the 4% Rule, we would need only $208,750 set aside $8,350 to cover our annual bucket list costs (25 x $8,350 = $208,750). Notice that the lower the costs in your retirement, the lower the need to have a passive income base.

Pensions and Social Security can have a significant impact on the income estimates. Assuming that you are able to draw funds from these sources around age 62, you will have an additional safety margin in your retirement.

I hope that you can see how the planning can get quite complex trying to match up purchases, travel, and other costs with the flow of income. If we were to go on a YOLO bender the first year of retirement, we would need to dramatically draw down a combination of savings and retirement accounts or—worst case—borrow money. So, we need to work out a smooth path to enjoy the activities we plan for the rest of our retirement.

Bottom line: If the balance of your passive income source today is greater than your estimated post-work expenses, you have reached financial independence.

Why not simply use FIRECalc or other online retirement calculators?

Many financial retirement calculators look at only a few items in the early retirement calculation, such as your age or number of years you expect to be in retirement and the balance of your retirement accounts. They often ignore passive income, other income sources, and the timing of those funds becoming available to you. All these variables need to become part of your model, to help determine if your nest egg is enough and to provide some additional clues about the timing of the income needed to support those expenses.

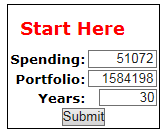

In the example provided, we estimate that, without Social Security and pensions, our balance needs to be $1,584,198 for a 30-year retirement. Using those numbers, here are the only three inputs required by FIRECalc.

The FIRECalc Results

Your spending in every year after the first year will be adjusted for inflation, so the spending power is preserved.

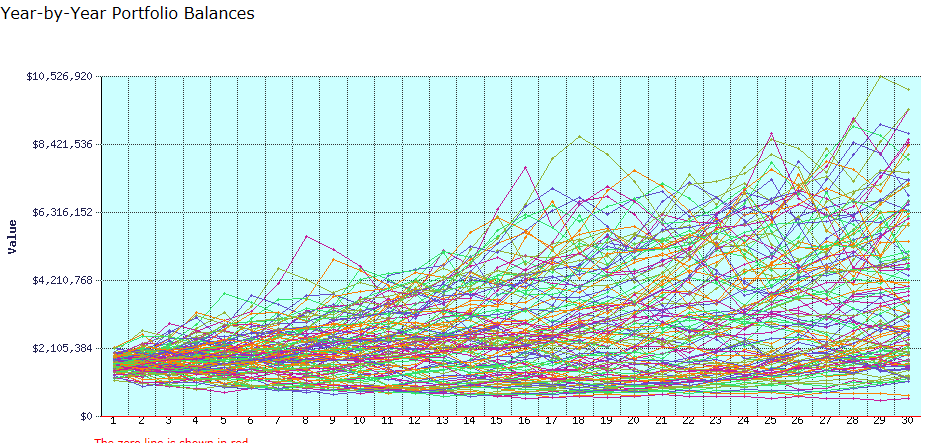

FIRECalc looked at the 115 possible 30 year periods in the available data, starting with a portfolio of $1,584,198 and spending your specified amounts each year thereafter.

Here is how your portfolio would have fared in each of the 115 cycles. The lowest and highest portfolio balance at the end of your retirement was $539,751 to $10,110,900, with an average at the end of $3,914,153. (Note: this is looking at all the possible periods; values are in terms of the dollars as of the beginning of the retirement period for each cycle.)

For our purposes, failure means the portfolio was depleted before the end of the 30 years. FIRECalc found that 0 cycles failed, for a success rate of 100.0%.

Note: FIRECalc bases its estimate on a portfolio of 75% stock index and 25% bond funds, with a 0.18% fee to the fund.

The results indicate that after drawing $51,072 a year and adjusting for inflation we will have an ending balance from $539,751 to $10,110,900. Wow! It appears that we have all that is needed if we stop working right now. Can that possibly be right?

FIRECalc, like other calculators, does not necessarily allow for multiple and diverse income sources such as business income, side hustles, part-time work, pensions, and annuities. The challenge for me is how do you place a value on rental real estate? I have based our own personal calculations on what the safe annual cash flow will return from those business operations. Retirement calculators have difficulty allowing for multiple passive income streams, periodic expenses, and early retirement scenarios.

We created a model to determine THE number.

We now know where the income is coming from and what the anticipated expenses are for a 30-year retirement. The spreadsheet is a model we created to indicate how one knows when he or she achieves financial independence and the impact later, when additional income sources such as Social Security become available.

We determined how much is enough. In this case, $1,584,198 is required to pay for a $51,072 a year lifestyle. We have smoothed all these numbers out for replacement costs, bucket list items, and have not considered the effects of inflation. These estimates are derived from a conservative 3% withdrawal rate. At a 4% rate, we would need $1,201,800 set aside today to reach the Financial Independence Number.

The example we provided shows that we have enough to retire based on either a 3% or a 4% withdrawal rate with a zero percent chance of running out. Why not retire now since the examples state financial independence has been achieved?

We will have the opportunity to review this in our article regarding what it takes to make the final leap toward retirement. Please check back for “Step 7: Retirement” next week.

Hey Bryan, great post. I really like this series.

Only question I have is, why for the 4% withdrawal scenario is the required amount put away less than the 3%? Shouldn’t this be the other way around? For 4% withdrawal, we should need more…

Thanks, Erik

Erik,

Thanks for the feedback on the series and the concern about the math. You got me thinking about it and I believe the math is correct.

Let’s use a different example that it takes $40,000 per year in income to support your lifestyle. Here is the math: $1,000,000 x 4% = $40,000. If you used 3% the math would be: $1,333,200 x 3% = $40,000 (rounded). You can see that using the more conservative 3% withdrawal rate means you need to have saved $333,200 more ($1,333,200 – $1,000,000).

The other approach is to take the 4% rule by multiplying 25 x $40,000 to arrive at a $1,000,000 nest egg needed to retire. The 3% rule is 33.33 x $40,000 to equal $1,333,200.

Please do let me know if my calculations are wrong.

Take care!

Ah! Ok, I see what I was thinking about. I wasn’t keeping the desired level of income constant. I had it backwards, I was looking at it like, if we had the same $1,000,000 investment nest egg, then to withdraw 3%, it would be taking out less capital. Just a mix-up on my part.

Thanks for clarifying!

Erik

YOLO Bender!!! 🙂

Great coverage on a complicated topic! I learned a lot!

Luke – I told you I was going to steal your term “YOLO Bender! 🙂 Check our “glossary” if you have not already done so.

Thanks for the kudos and I am glad this article was helpful.

I enjoyed the post. My problem is still doing mental jumping jacks trying to figure out my FI number. I know we focus on the spending side of thing, but FI to me has to be without the mortgage and the rest of this debt gone. Then I can adjust my spending as of right now, but it is still a bit in precise, particularly when I consider what prices will be in a few years. Maybe I need to go back and look at these calculators. But then I do mental jumping jacks is if I should pay off the house before I save so that I can get a quicker to the FI money. Or maybe I just need to focus….

Thanks for sharing your thoughts with us. We too struggle with trying to understand our FI number and where to place our focus. You are not alone my friend!

We went through the “mental jumping jacks” ourselves when we paid of our home mortgage that we shared in this article. Should we pay off most of the rental real estate debt that has a similar interest rate as the home mortgage and then would free up more cash flow, or do we pay off the personal home mortgage that has too little amount of interest to itemize on our taxes?

Now six months has passed since paying off our home and we hardly think about it anymore!

I had the same question as Erik above. I understand by your explanation how you reached the higher 3% number than the 4% number, but I think it is a little misleading. Shouldn’t your fixed amount be the amount you can save? So, for example, you need $1,000,000. At 4%, you will live off of $40,000 per year. However, you think you can live off of 3% = $33,000 per year. $33,000 per year x 25 years is only $825,000 total that you need.

Again, I understand that you were keeping constant the $40k that you need to live off of per year, but this is just how I read it.

Anyway, another good write up! I like the detail you provide in your posts.

-DP

Thanks for the feedback and the questions DP. I love that our readers keep us honest here!

My example to Erik was meant to show that when you apply the more conservative 3% Rule you would need to have saved more than if you are drawing funds at a 4% rate.

In our example of expenses, we felt we need $51,072 a year to pay for our lifestyle. Of this $51,072, we expected that we would earn $5,000 per year doing some part time employment. So I was working from that constant annual expanse amount of $46,072 to arrive at $1,534,198 for 3% ($46,072 x 33.33) with some rounding or $1,151,800 for a 4% withdrawal rate ($46,072 x 25).

The good news is that with either approach, we could afford to leave our employers right now!